At Masou, we are long term, bottom-up, equity investors. We named our business after the anadromous Masou salmon because we believe that if we are to achieve superior returns, we must have the courage to swim against the tide. We scour Asia Pacific for the most compelling investment opportunities, irrespective of prevailing market sentiment, logistical challenges or langauge barriers. By blocking out the noise, we are able to focus on the factors that drive long-term investment returns:

Investment philosophy

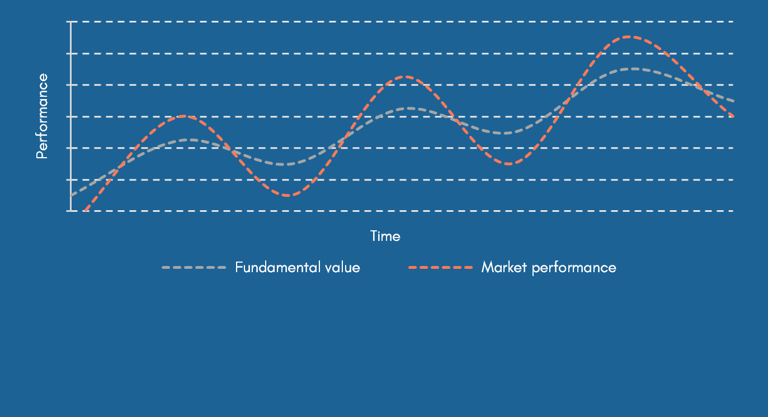

Stock market performance mirrors fundamental performance over the long term, but the two can diverge significantly in the short term

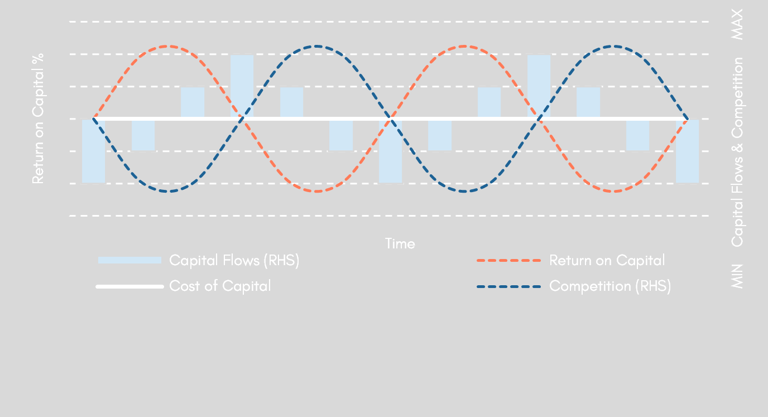

Profitability is inversely correlated to competition and therefore tends to mean revert

Sensible, and at times contrarian, capital allocation can enhance the rate at which companies compound fundamental value

The price paid for an investment has a significant bearing on its likely contribution to the return of the portfolio as a whole

Our philosophy often leads us to segments where profitability is supressed, capital investment is declining and consolidation is ocurring. Our interest is also piqued by companies undergoing restructurings, especially where there has been management change. Our research is not however limited to companies achieving low absolute levels of profitability. We weigh a company’s current returns against historic returns, competitor returns, the cost of capital and the competitive environment.

Quantitative analysis and company interactions help us build a more informed view of a company's strengths, weaknesses, opportunities and risks. We compare our findings against the market valuation of the company.

Investment process

We assess the quality of the company's:

We evaluate the company's potential to grow fundamental value via improved:

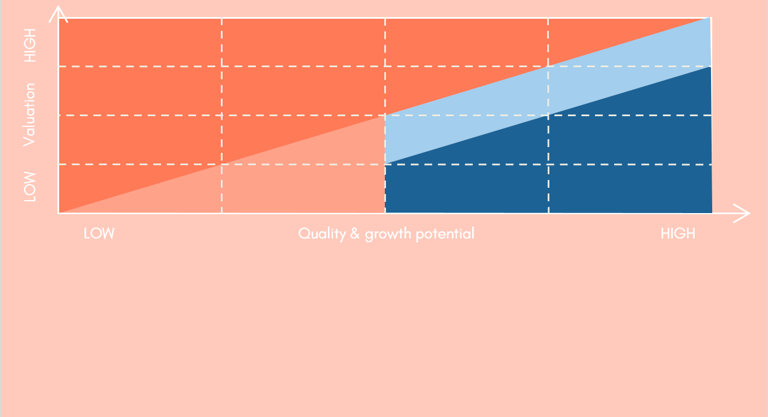

We seek a meaningful spread between our assessment of a company's quality, growth potential and its market valuation

We see a portfolio that is highly diversified and constructed in a bottom-up, benchmark agnostic fashion as the most effective means of expressing the conviction we have in our investment beliefs. Our portfolio looks and performs differently to our regional benchmark and many of our Asia-focussed peers.

Our diversified approach reduces the degree of idiosyncratic risk, allows us to take on opportunities with potentially higher returns outcomes and deploy more capital into niche areas. We believe diversification also limits the potential for overconfidence and endowment biases to take hold.